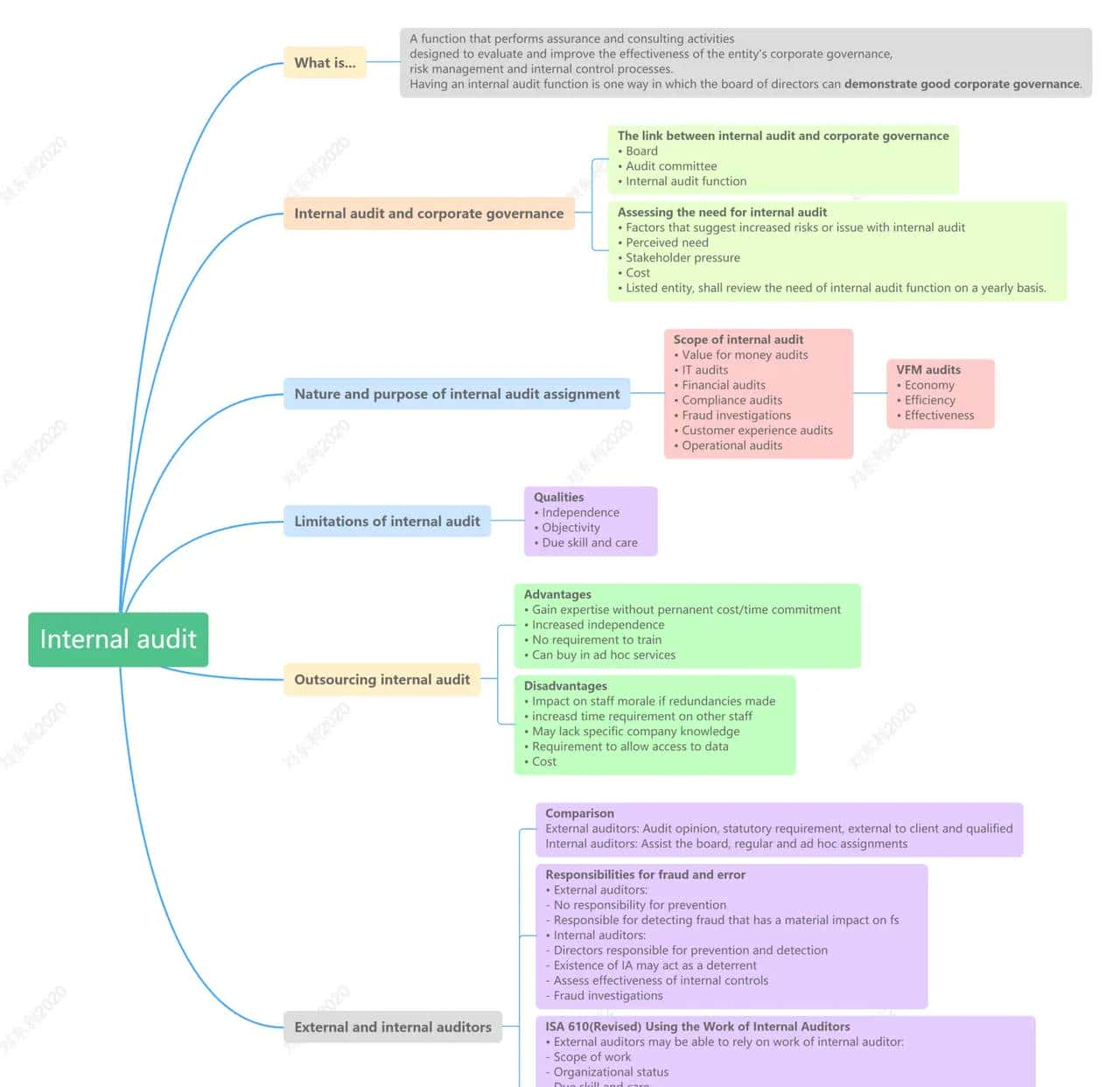

The internal audit function (or department) is a function established by management and those charged with governance of an entity to assist in corporate governance by assessing internal controls and helping in risk management. It can be a department of employees or can be outsourced to expert service providers.

Internal auditing is different from external auditing, although the techniques used by each are very similar. While the techniques used may be similar, the focus and reasons behind the audit are different.

We will consider what the internal audit function is, what they do, and the key differences between the internal and external auditors. It is very important to know these differences as the roles are distinct, and you may see questions on the rules and the differences between them in the exam.

The role of internal audit is far more varied than that of external audit, and we will see the various assurance assignments that may be undertaken by internal editors.

© 版权声明

文章版权归作者所有,未经允许请勿转载。

相关文章

暂无评论...