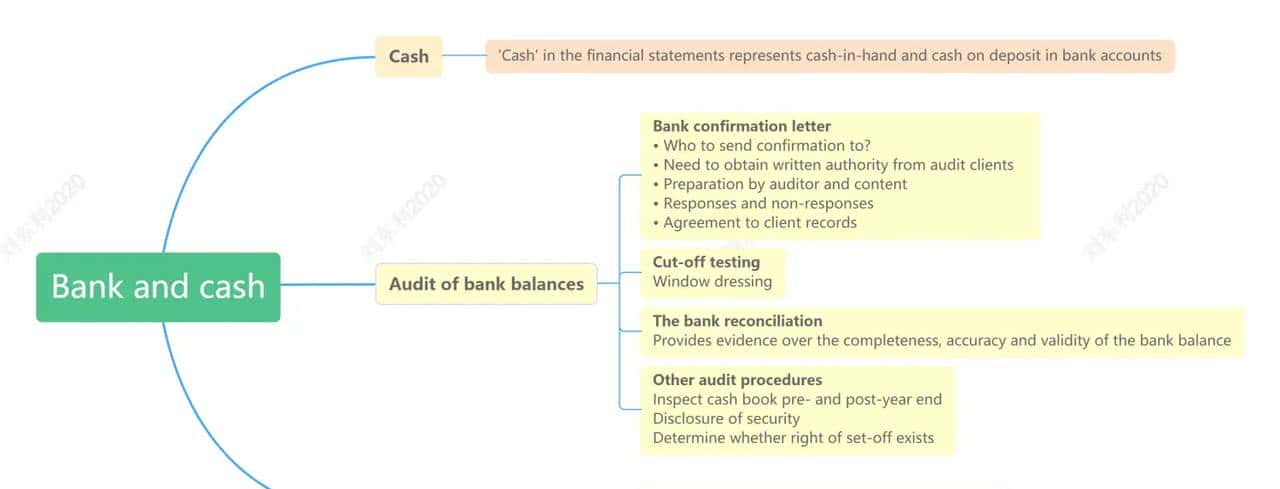

Work on cash and bank will concentrate on the completeness and valuation assertions using the bank reconciliation, bank confirmation letter and counting of cash as key audit tests.

In the exam you may be asked to identify and explain audit procedures you would perform to confirm specific assertions relating to cash and bank. Shorter constructed response question requirements and OT questions in Section A may also ask for audit procedures specifically used to obtain bank confirmation letters.

Remember that the bank confirmation letter contains the balance held by the client at the bank per the bank s record. This must be reconciled to balance held with the bank per the client s record. When suggesting audit procedures for verifying bank balances, although the bank confirmation letter is important, do not forget to suggest other procedures related to the year-end bank reconciliation. Previous candidates have lost out on marks for not focusing enough on these procedures.

© 版权声明

文章版权归作者所有,未经允许请勿转载。

相关文章

暂无评论...